Expanding to India is a strategic lever for Australian businesses. It offers scale, talent, and cost efficiency. However, the regulatory landscape is unforgiving.

As a Chartered Accountant advising Australian CFOs, I see many get stuck in the “verification loop” because they miss specific cross-border requirements.

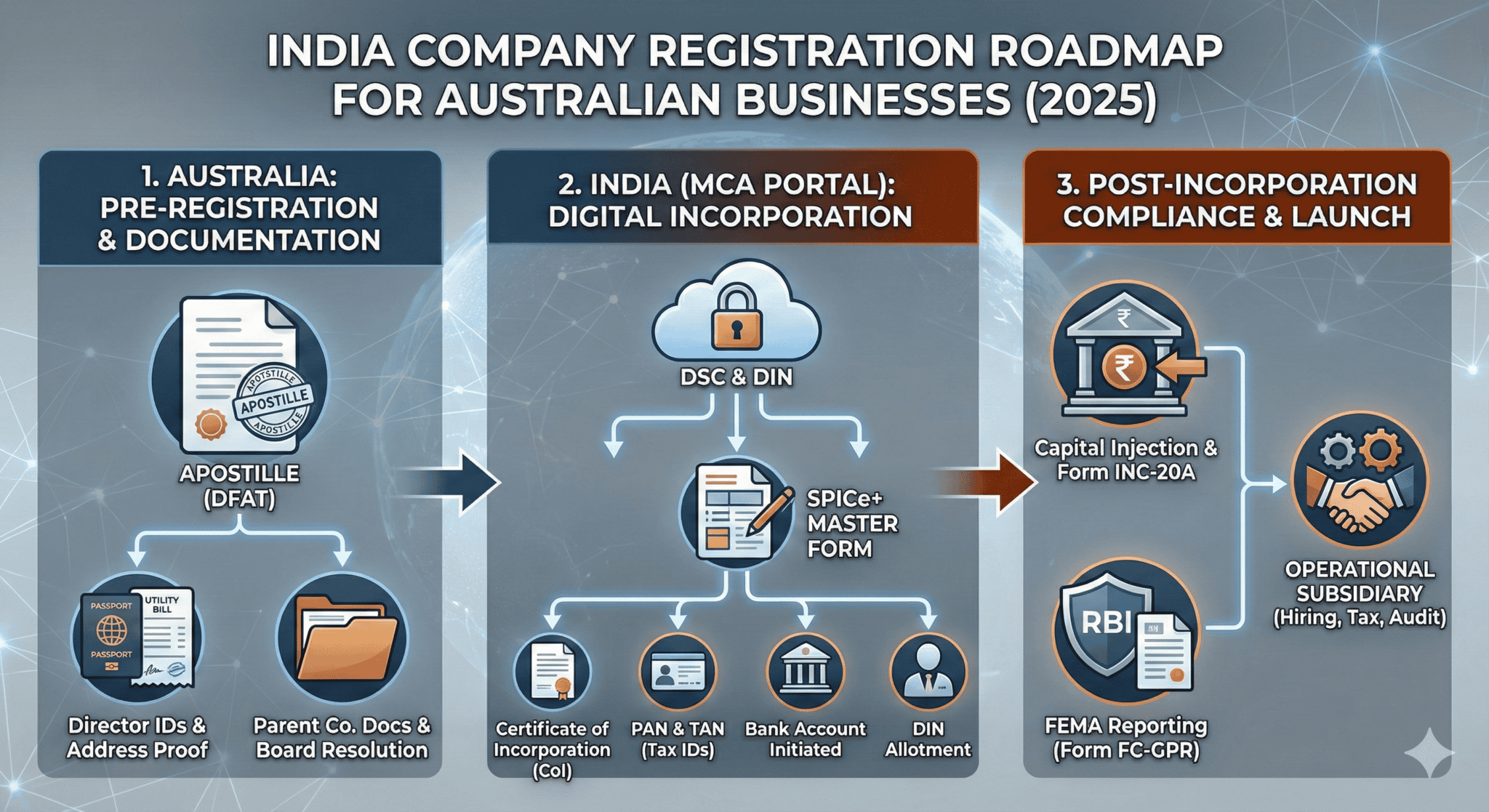

This guide cuts through the noise. It details the exact documents, timeline, and compliance required to incorporate your Indian subsidiary efficiently.

Table of Contents

Toggle1. The Pre-Requisite: Documentation & Verification

This is where 90% of delays happen. Indian authorities do not accept standard Australian photocopies.

The “Apostille” Rule

Since Australia and India are Hague Convention members, your documents must be Apostilled by the Department of Foreign Affairs and Trade (DFAT) in Australia.

Checklist for the Australian Parent Company (Shareholder):

Certificate of Incorporation: Certified and Apostilled.

Memorandum & Articles (Constitution): Certified and Apostilled.

Board Resolution: A formal document authorizing the investment, signed by the Australian directors. (notarised and appostilled)

Checklist for Directors:

Foreign Directors: Passport and Address Proof (Bank Statement/Driver’s License) – Apostilled.

Indian Resident Director: PAN Card and Aadhaar Card.

Note: You are legally required to have one director residing in India.

2. The Registration Process (Digital & Centralised)

Registration is handled by the Ministry of Corporate Affairs (MCA). The process is fully online.

Step 1: Digital Identity (DSC & DIN)

We generate a Digital Signature Certificate (DSC) for all directors. This is the legal equivalent of a wet ink signature. Once active, we apply for a Director Identification Number (DIN).

Step 2: Name Reservation

We reserve your corporate name.

Strategy: Use your Australian brand name with “India” suffixed (e.g., TechOz India Pvt Ltd). If you hold the trademark in Australia, provide the trademark certificate to secure the name instantly.

Step 3: The SPICe+ Filing

We file the SPICe+ (Simplified Proforma for Incorporating Company Electronically). This single “Master Form” accomplishes five things at once:

Incorporation: Issues the Certificate of Incorporation (CoI).

PAN Issuance: Your corporate Income Tax ID.

TAN Issuance: Your Tax Deduction Account Number (for payroll).

DIN Allotment: For new directors.

Bank Account: Automatically initiates a current account opening with your chosen bank.

3. Post-Incorporation: The “danger Zone”

Incorporation is not the finish line. You must complete these three steps immediately to avoid penalties or being struck off.

Appoint an Auditor (Form ADT-1):

Deadline: Within 30 days.

Action: Appoint a practicing Indian Chartered Accountant to audit your financials.

Capital Injection & Commencement (Form INC-20A):

Deadline: Within 180 days.

Action: Transfer the share capital from your Australian bank to your new Indian bank account. We then file Form INC-20A (Certificate of Commencement of Business).

Warning: You cannot legally conduct business or hire until this form is filed.

FDI Reporting (Form FC-GPR):

Deadline: Within 30 days of receiving money.

Action: Report the foreign investment to the Reserve Bank of India (RBI). Failure to do this attracts massive compound interest penalties.

4. Hiring & Taxes: What Australian CFOs Must Know

Double Taxation Avoidance Agreement (DTAA)

India and Australia have a robust DTAA.

Corporate Tax: Starts at 15% for new manufacturing units; roughly 25% for service sectors.

Repatriation: Taxes paid in India can typically be claimed as a credit against your Australian tax liabilities.

Employment Contracts

Indian labour law is employee-centric.

Notice Period: Standard is 30–90 days (not 2 weeks).

Provident Fund (PF): Mandatory retirement contribution (12% of basic salary) for companies with 20+ staff.

Leaves: Mandatory paid leave rules differ by state (e.g., Karnataka vs. Maharashtra).

Summary

Registering in India is a predictable, systematic process if you respect the documentation requirements. The key is to get your DFAT apostilles sorted early and ensure your RBI filings are precise.

Can an Australian company own 100% of an Indian company?

Yes. Under the Automatic Route, 100% Foreign Direct Investment (FDI) is permitted in most sectors without prior government approval.

Is a physical office required in India?

Yes. You must have a registered office address in India to receive official correspondence. However, you may use a virtual office service for the initial registration.

What is the minimum capital requirement?

There is no minimum capital requirement